Company liquidation Estonia: a practical guide to closing your OÜ compliantly

Company liquidation Estonia is the formal process of closing an Estonian company (most often an OÜ) so it can be cleanly deleted from the Commercial Register and you can move on without lingering compliance duties. In 2026, getting the steps and timing right matters more than ever, because missed filings, unfinished tax matters, or unclear asset distributions can create avoidable follow-up risks.

If you want a structured, “done-right” exit, Silva Hunt (an Estonia-based legal, tax, and accounting team) can manage the full process as a packaged service, including the legal filings and the accounting deliverables required during liquidation.

What “Company liquidation Estonia” means in practice

In Estonia, liquidation is a regulated winding-up procedure. Once shareholders decide to dissolve the company and a liquidator is appointed, the company’s status changes to “in liquidation” (OÜ likvideerimisel). From that point, the company should stop normal business expansion and focus on closing properly: notifying creditors, settling liabilities, completing tax duties, preparing liquidation accounts, and applying for deletion from the Commercial Register.

A compliant Company liquidation Estonia process typically aims to achieve three outcomes:

- Limit future liability exposure: once deleted, the company no longer has ongoing filing obligations.

- Debts are properly handled: creditors have a clear claim window and liabilities are resolved.

- Transparent distribution of remaining assets: shareholders receive liquidation distributions after all obligations are paid.

Company liquidation Estonia timeline: why it often takes 8 – 10 months

A common reason founders underestimate Company liquidation Estonia is the mandatory creditor claim period. After the liquidation notice is published in Ametlikud Teadaanded (Official Announcements), creditors must be given at least 4 months to submit claims. You cannot rush past this waiting period if you want a clean deletion.

In real life, the end-to-end timeline often lands around 8 – 10 months because you also need time to:

- close contracts, collect receivables, and sell or transfer assets (if needed)

- complete accounting and tax filings through the last periods

- prepare and approve the final liquidation report and balance sheet

- file the deletion application and wait for registry processing

Company liquidation Estonia: step-by-step process

Below is the standard voluntary liquidation flow (the core steps are the same whether the owners are local or e-residents):

1) Shareholders’ resolution to liquidate

- Adopt a decision to dissolve (often 2/3 majority, unless your Articles require more).

- Appoint liquidator(s).

- Prepare the shareholders’ decision, updated shareholder list, and liquidator’s consent to act.

2) File the liquidation entry with the e-Business Register

- Submit the dissolution application and liquidator appointment.

- Status changes to “in liquidation”.

3) Publish the liquidation notice (Ametlikud Teadaanded)

- Notice is published in the official announcements portal.

- The minimum 4-month creditor claim period starts.

4) Notify known creditors directly

Send written notices to creditors you already know about (best practice in addition to public notice).

5) Prepare the opening liquidation balance sheet

Establish the company’s financial position as liquidation begins.

6) Terminate business activities

- Conclude contracts.

- Collect receivables.

- Sell assets if needed to settle obligations.

7) Settle liabilities

- Pay creditors.

- Resolve disputes.

- Handle employee terminations (if applicable).

8) Tax compliance (critical in Company liquidation Estonia)

- File all required tax returns (VAT, payroll, corporate distributions if any).

- Settle outstanding liabilities.

- Deregister from VAT if applicable (and manage any VAT-on-assets consequences on deregistration).

9) Prepare the final liquidation report and distribution plan

- Final balance sheet.

- Asset distribution proposal.

10) Approve final report and asset distribution

Shareholders approve the final documents and distribution plan.

11) Distribute remaining assets

Distribute only after the creditor claim period ends and liabilities are settled.

12) Submit deletion application to the Commercial Register

Liquidator files the deletion application with the required annexes (final balance sheet and asset distribution plan).

13) Retain documents

Keep accounting and key company records for the statutory retention period (often 7 years, depending on the document type and legal basis).

Taxation in Company liquidation Estonia: retained earnings vs share capital

Tax is often the most misunderstood part of Company liquidation Estonia, especially for remote founders who assume “closing” means “no taxes.” Estonia’s corporate income tax is generally triggered when value is distributed out of the company.

Retained earnings paid out during liquidation

If liquidation proceeds include previously untaxed retained earnings, they are generally treated like profit distributions and taxed at the company level using Estonia’s standard corporate income tax method: 22/78 of the net distribution (as applicable in 2026).

Returning paid-in share capital (often tax-free if recorded correctly)

In many cases, paid-in share capital can be returned to shareholders without corporate income tax – if it was properly registered/declared and the repayment does not exceed the documented paid-in capital. The e-Residency knowledge base explicitly highlights that declaring share capital correctly helps you pay it out tax-free when closing.

Practical takeaway: in Company liquidation Estonia, the difference between “profit” and “capital” is not just accounting language it can materially change the tax outcome, so documentation and correct register/tax declarations matter.

What if my company is VAT-registered?

If your company is VAT-registered, liquidation often involves VAT deregistration. Estonia’s Tax and Customs Board notes that when a taxable person is dissolved and the tax authority receives notice, they can be removed from the VAT register; there may also be obligations on certain goods/assets where input VAT was deducted.

This is one of the areas where founders commonly run into issues late in liquidation (for example: assets still on the balance sheet, unfinished invoices, or late VAT returns). Handling it early keeps the liquidation timeline predictable.

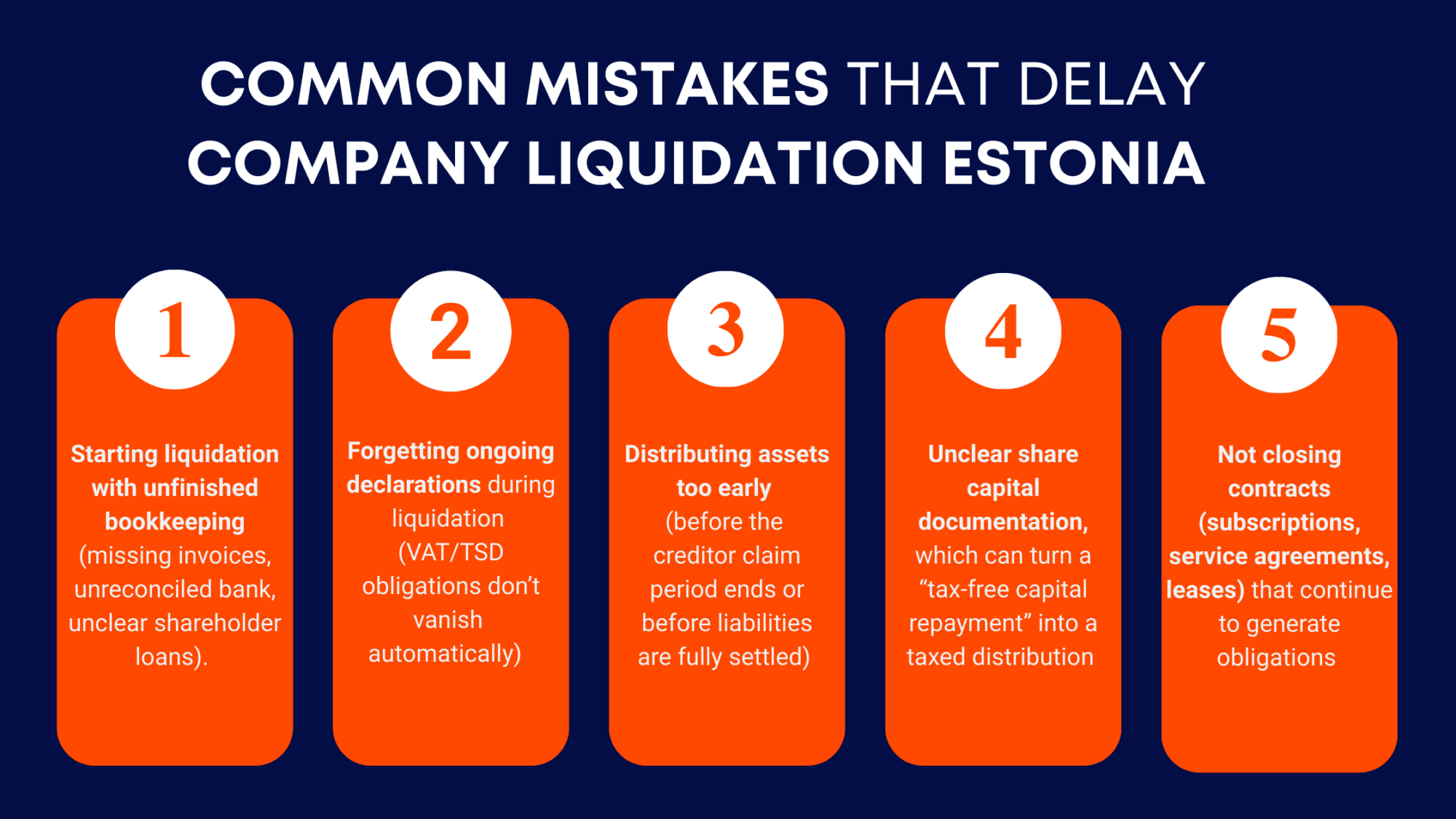

Common mistakes that delay Company liquidation Estonia

Common mistakes that may lead to delays

- Starting liquidation with unfinished bookkeeping (missing invoices, unreconciled bank, unclear shareholder loans).

- Forgetting ongoing declarations during liquidation (VAT/TSD obligations don’t vanish automatically).

- Distributing assets too early (before the creditor claim period ends or before liabilities are fully settled).

- Unclear share capital documentation, which can turn a “tax-free capital repayment” into a taxed distribution.

- Not closing contracts (subscriptions, service agreements, leases) that continue to generate obligations.

How Silva Hunt supports Company liquidation Estonia end-to-end

Silva Hunt’s liquidation service is designed for founders who want a compliant, clean exit without chasing deadlines, registry notices, and accounting deliverables across multiple providers.

In practice, the appointed liquidator works together with Silva Hunt’s Accounting Department to handle:

- preparation of the shareholders’ decision pack and registry filings

- official submissions (reports, balance sheets, required annexes)

- creditor notice monitoring and claim handling workflows

- tax filings and, if needed, VAT deregistration coordination

- final report, distribution plan, and deletion application

Because Company liquidation Estonia is both a legal and accounting process, having one coordinated team reduces “handoff risk” (where something gets missed between a lawyer, accountant, and founder).